In case you missed it... Cost of Capital Differences Deepen | The Bengal Bite 🐯

Green Thumb Industries (GTI) gave everyone yet another reason to become familiar with its name (looking at you Jim Cramer) recently by finalizing a $217m senior debt financing on April 30 - $105m to pay back other debt, the balance for expansion, and an additional $33m that could be drawn over the next twelve months. Larger amounts have been raised in cannabis before, but a few things stand out about this particular raise that investors should notice: the interest rate is 7% (likely the lowest of any U.S. MSO capital raise of this magnitude), the warrant coverage is modest, and the raise was non-brokered so GTI did not have to engage an investment bank to source the majority of the money.

GTI’s raise also shows the widening gap in the cost of capital between the bigger players and the smaller ones, potentially spurring even greater levels of consolidation. Comparing the debt GTI is paying off with the debt it is now incurring quickly shows how far and fast its cost of capital has fallen:

Source: Bengal Capital market research

What investors charged GTI for capital effectively halved over two years, but also has come down to absolute levels that not many would have predicted back in 2019 - 7% is a moderate interest rate in many industries.

Compared to smaller public cannabis companies, GTI is also significantly ahead of the curve: Cansortium, a much smaller public cannabis company, just raised $71m at an effective rate of 14%+ with similar warrant coverage. The gap is typically even wider for private companies, although some have been slow to realize it as they anchor on the press releases of much larger public companies as a guide for what their capital should cost.

A lower cost of capital is a significant advantage to a business: it allows the business to invest in more potential projects which generate a return above that cost of capital. If investors lend me money at 13%, I better be getting more than 13% out of whatever I put it into. 7% is obviously easier to make than 13%, leaving some combination of more return for the equity owners of the business, greater amounts of capital to invest in high-returning projects, and an ability to share the savings with customers and employees, helping to build greater market share and engagement.

And in simple terms, as the cost of capital advantage deepens, it becomes much more logical for smaller companies to join up with GTI rather than fight against them - if GTI is so good at raising capital, why not just become a part of GTI and then raise the money together vs. trying to raise it all on your own and getting diluted as investors demand much higher rates? And it can make sense for GTI to be more acquisitive because, if the market is rewarding size with a lower cost of capital, it pays to be bigger. Rinse, repeat.

At the time of this writing, the raise is still fresh and it’s unclear whether it will have any effect… just kidding, GTI announced an acquisition in Virginia four days after the raise.

This Week's Bite:

CANN cans cannabis for the masses: People are starting to hear, and feel, the buzz around the cannabis beverage brand, CANN. With only 2.5mg of THC per beverage, CANN is not geared towards medicinal or high-tolerance consumers, and has its sights instead set on the average White Claw drinker -- “the healthy hedonist.” CANN co-founder Luke Anderson said, "We’re going after consumers who never purchased cannabis from a dispensary before.” It turns out there are quite a few of these consumers in California—CANN now controls the largest share of the beverage market at 25% of overall revenue. With their robust DTC platform and mainstream appeal thanks to celebrity endorsements from Ellen DeGeneres and Gwenyth Paltrow, CANN seems to have found their canna-curious consumers. (Forbes)

Source: Forbes

Carbon cap for marijuana? In order to sell legal cannabis in any given state, you must also source cannabis from said state. That means that when you need to grow cannabis in places as humid as Hawaii or as cold as Maine, you have to heavily rely on indoor, climate-controlled grows that are not energy efficient. More scrutiny is being placed on the nascent cannabis industry with advocates pushing for more environmentally friendly regulations. (Rolling Stone | Hemp Industry Daily)

Source: Dan Page for Rolling Stone

Philip Morris eyes cannabis opportunities: Tobacco companies in many ways are a natural fit for the cannabis industry: 1. They know how to operate in a regulated environment, 2. They have experience consistently growing a crop, and 3. They have advanced vaporization technology. In a recent interview, Phillip Morris’ CEO Andre Calantzopoulos said they are weighing the potential of a future cannabinoid-based offering. “We are doing all this work and will determine one day what avenues to pursue. But our priority is what we’re doing with our smoke-free products.” It will be interesting to see how any future cannabis investment will compare with Altria’s existing investment in Canadian licensed producer Cronos and British American Tobacco’s recent investment into Canadian licensed producer Organigram. (Financial Post | Bloomberg)

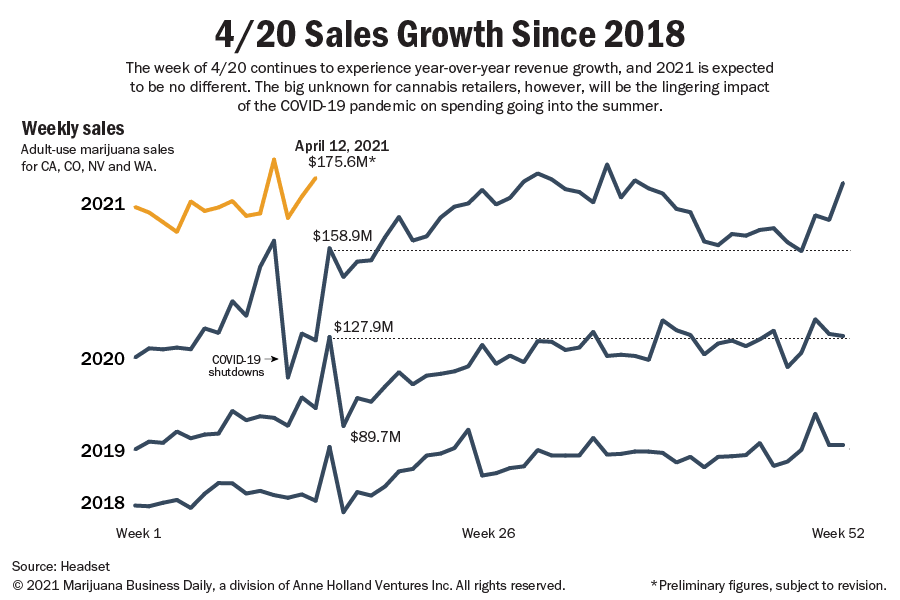

4/20 makes a comeback: 4/20 sales for 2020 were middling at best due to the timing of national pandemic lockdowns. Consumer demand was accelerated as people stocked up anticipating cannabis stores being shut down, reducing some of the importance of the shopping day. However, the sales holiday made its comeback in 2021. A new one-day sales record was hit with over $111m worth of cannabis sold across the United States on 4/20 alone, according to cannabis data firm Akerna. Interestingly enough, while 4/20 is often the best sales day of the year, the week before and after generally are among the worst sales weeks for the cannabis industry. (Marijuana Business Daily | Fortune)