Position of Strength

Our Guess on Why GTI Didn't Rush to Get a Refund

Interim Fund Update

The Bengal Catalyst Fund’s current estimated net returns, not including side pockets, through close of business Friday, June 7, 2024 for Q2-to-date are below:

We are pleased with our concentrated portfolio’s performance, as well as its positioning for continued long-term capital appreciation.

Additionally, for those interested, Bengal Capital partner Jerry Derevyanny was recently a guest on the Seeking Alpha Cannabis Investing Podcast where he discussed some of his views on cannabis investing. Jerry will also be appearing on HedgeyeTV this coming Thursday, June 13, at noon EST/9am PST. Bengal Partner Josh Rosen recently appeared on HedgeyeTV as well in a cannabis fireside chat with Howard Penney which can be accessed here.

Not Quite A Hail Mary or a Forced Move, But Still Not Great

Once, in his somewhat wayward twenties, a particular Bengal partner was spending time with friends telling ribald stories and shooting tequila when another friend entered the party, sat down,and triumphantly announced that he had made $1,000 that very day (a not insignificant sum to those present). In the hushed pause that followed someone finally asked how he’d done it.

Well, he announced, it was really quite simple: he had been importing counterfeit Spyder ski coats from China and selling them as authentic on eBay. The US Customs Service had found out and issued him a fine of $1,200. But, he had called the Customs Service, cried (literally) on the phone and begged them that he would never do this again, so they had knocked the fine down to $200 because it was his first offense. Looking like a fox that had swallowed an entire chicken, he took another generous shot of tequila.

Calling the Customs Service and getting the fine reduced was the best move to make in his situation but it was more than fair to have some serious questions about how he got into that situation in the first place. And so it is with the recent spate of large MSOs’ tax refunds. Except, unlike many cannabis investors apparently, the friends deep into their cups instantly recognized that the eBay entrepreneur had performed something closer to a forced move/hail mary than a genius stratagem. Even more bewilderingly, some cannabis investors do not even seem to recognize that a company not asking for the tax refund (notably, GTI) is a sign of strength, not cheaping out on tax lawyers.

What, Why and Why Now

Many MSOs have filed amended tax returns for prior years, some of whom have received substantial refunds - i.e., effectively claiming they overpaid taxes in those years. Trulieve started the trend, announcing amended returns claiming overpayment of $143 million and receiving $113 million in refunds on its Q4 2023 earnings call. Curaleaf, after being asked about Trulieve’s tax refunds on their Q4 2023 earnings call and saying that “Curaleaf is taking the position of paying all of our taxes,” opened their Q1 2024 call by announcing that “[w]e also anticipate amending certain prior year returns to claim refunds of excess federal income tax that was paid based upon application of Section 280E.” And so on, with GTI being one of the few that has stayed silent.

We highlight GTI’s answer to a question about refunds in its Q1 2024 call as a near textbook example of saying “We’ll wait and see and not stick our necks out” in pristine businesspseak: “So at this time, we continue to assess the landscape and watch what's happening in the marketplace, while we make a determination of what we're going to do next. So we continue to toe the line at this junction while it evolves to be able to determine what ultimately our next steps are.”

GTI’s absence actually caused some investor consternation and criticism - how could GTI not follow the same path of obtaining free money from the government? Many investors mistakenly believe that receiving a refund is tantamount to the IRS approving the refund without ever stopping to consider why, if this were in fact the case, companies are now booking uncertain tax positions on their balance sheets. Despite cannabis companies’ generally poor disclosure, here investors are refusing to believe what the companies themselves say in black and white: there’s a good chance that they will need to give these refunds back. And potentially more in penalties, not to mention the time, distraction, and cost of audits and tax controversies.

Invariably, the companies going through with this have relied upon a tax opinion backed by a decently sized law firm. In our view, the principal purpose of the tax opinion is not because of confidence in the ultimate success of the opinion, but rather so long as the opinion is considered reasonable (it can be both low probability and reasonable based on certain precedent), then certain punitive penalties regarding improper refunds become much less likely.

The reason why many companies did this is not hard to divine: the risk/reward is clearly positive given the state of their balance sheets. If you’re a major MSO with a stressed balance sheet that can get an even temporary reprieve by using a tax refund in this market or the request for a refund that allows you to stop paying 280E taxes going forward, you’ll do it because there are roughly two outcomes: the IRS will want it back, or you can keep it. If the IRS wants it back, that will be a process that likely takes a few years. A few years from now, hopefully Florida has gone rec, SAFE is passed, Schedule III is finalized, etc., and this little tax liability is a rounding error. Or, if those things don’t happen, the gargantuan debt default problems are going to dwarf the pesky IRS looking for its refunds back anyway.

To return to what is truly mystifying about the whole situation is investors not realizing that the company that can afford to sit back and coolly watch everyone else do this is doing better.

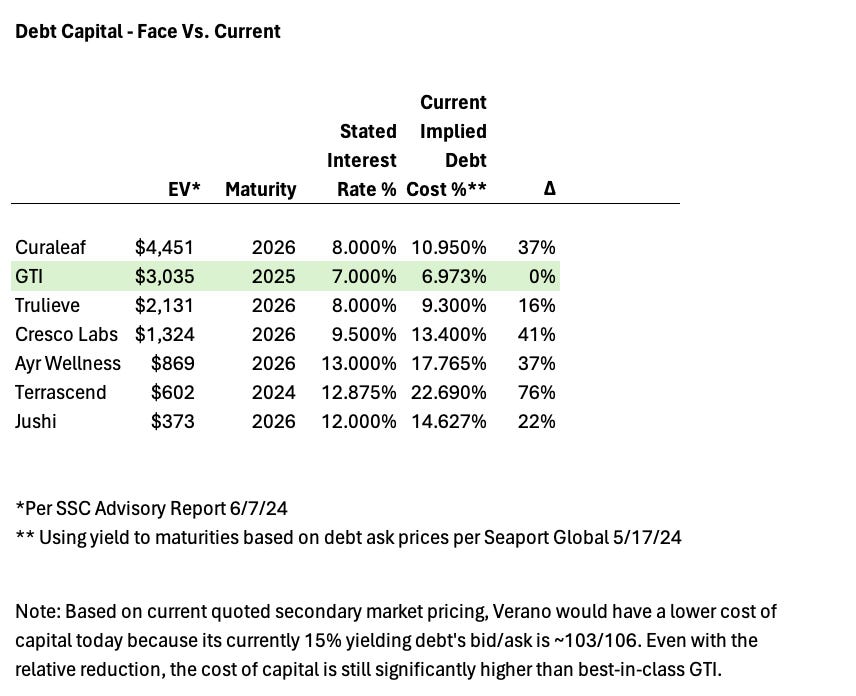

Current Debt Costs

You can generally get a quick read on what current debt costs of capital are by seeing where companies’ debt trades; cannabis debt markets aren’t that liquid/deep, but still a reasonable proxy. So, if a company issued 8% debt that now trades at a slight discount so a purchaser would get a yield of say 10% on it, then you can roughly say that if that company had to refinance that debt today, they would need to offer a 10% or higher interest rate. While almost everyone else’s debt capital costs have gone up, GTI’s has stayed roughly the same. And, GTI’s current rough cost of debt capital is at or below what the IRS itself currently charges for interest: 8%. So why play audit roulette with the government if it doesn’t save you much (or anything) anyway?

We’re assuming GTI took the step to keep its prior tax years open through some type of appeal or protest, in order to prevent the three-year statute of limitations from kicking in, thus allowing them to go back and amend their tax returns should these new tax opinions prove successful - that’s just good business.

“Institutional Capital”

Without going too deep into this topic as it will likely be fodder for Bite in the near future, it is difficult to see even a first day analyst at a large mutual fund, i.e. “institutional capital,” looking at the comps below and not very quickly spotting an outlier.

Often cannabis investors treat “Tier 1” large MSOs as fungible and speak about them in general terms. This is unfortunate, because it’s much more likely that when institutional capital actually starts to look at the space, they will see large individual differences between the companies.

Let’s be real: large mutual and pension funds may pause at the thought of investing in a company where every eighth dollar of capital is either unpaid taxes or at least somewhat questionable tax refunds - cannabis or not.

Again, we hope to address the question of what “multiple” cannabis companies should trade at in a Bite soon.

So What?

Gladys Jennip: What is this about?

Nathan Muir: Money. Free trade, microchips, toaster ovens.

Gladys Jennip: And what does that have to do with you?

Nathan Muir: [to Gladys as he leaves the office] Nothing.

– Spy Game, 2001

That’s a lot of words we just wrote about a stock we don’t even own in the Fund, although a few Bengal partners have positions in their personal accounts, most as seed investors. The point here is, broadly, that the call is coming from inside of the building: there may not be so much mispricing of cannabis stocks as misunderstanding by cannabis investors as to what things are worth and why - the reaction to the tax refunds is just the latest data point. Another example is some cannabis investors’ negative reaction to the idea of a GTI merger with Sam Adams - something we hope to write about in the near future as well. We think a different way of thinking will lead investors to better results, and we practice what we preach in the Fund.

The quest for “high growth” stories has caused a mispricing of cannabis companies, like Grown Rogue, that are built on high incremental capital returns, which we have tried to take advantage of. But, unlike many other types of games, economic games allow both sides to win - for our companies to do well does not mean others need to do poorly. And it does not hurt us one bit if investors were to listen to us and start to shift their holdings towards more high quality larger cannabis companies while we continue to focus on smaller companies where we can add the most value.